Tecnologías como los vehículos eléctricos, las baterías o los equipos de energías renovables dependen en gran medida de un número reducido de países, y esta situación se mantendrá hasta 2030, dadas las inversiones ya comprometidas y la evolución actual del mercado.

Why it matters: Forces solar installers to build supply chain resilience beyond China or face perpetual price and availability shocks.

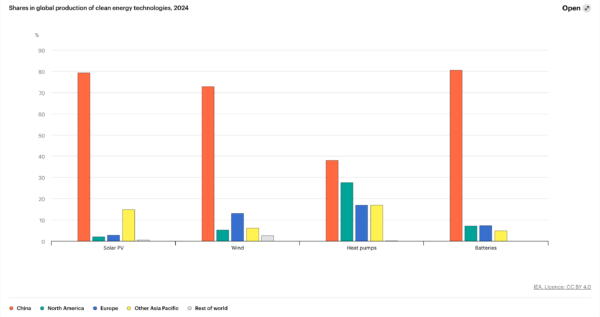

Why This Matters for European Solar Installers

This IEA warning isn't abstract geopolitics—it's a direct threat to your project timelines, pricing, and business stability. When China controls 85% of critical clean tech manufacturing, every European installer becomes hostage to a single supply chain. We saw this during the pandemic and shipping crises: module prices spiked 30%+, lead times stretched to 6+ months, and projects were cancelled or delayed. This concentration risk hasn't improved; it's structurally locked in until at least 2030.

Market Context & Implications

The EU's Net-Zero Industry Act and Critical Raw Materials Act are desperate attempts to build local capacity, but they're racing against a decade of Chinese industrial policy. While European manufacturers like Meyer Burger struggle, Chinese giants continue to dominate through vertical integration and massive scale. For installers, this means:

What Solar Businesses Should Watch For

Smart installers are already adapting. First, diversify your supplier portfolio—explore Southeast Asian production (Vietnam, Malaysia) and the emerging Turkish solar manufacturing base. Second, build stronger inventory buffers for critical components, even if it ties up capital. Third, communicate supply chain realities to customers upfront; transparency about lead times builds trust. Finally, watch the EU's 'resilience auctions' and local content requirements—these could create premium pricing opportunities for projects using European-made components, even at higher upfront costs.