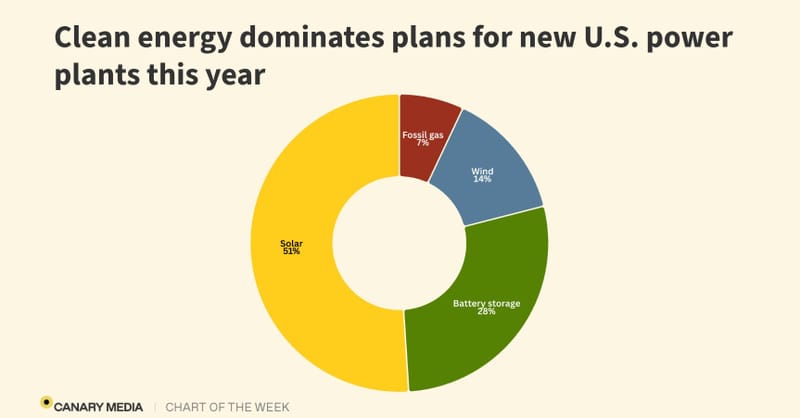

The U.S. is poised to build more solar and wind capacity in 2026 than ever before, with clean power projects overwhelmingly dominating the new generation pipeline.

Why it matters: Prepare for a tighter global supply chain and pivot your business toward high-margin energy management services to offset shifting market dynamics.

The Transatlantic Decoupling

While the US pipeline for 2026 is surging, European installers are facing a different reality: a 'post-boom' hangover characterized by inventory gluts and cooling residential demand. The US momentum is driven by the Inflation Reduction Act (IRA), which provides long-term investment certainty that Europe’s fragmented regulatory landscape still struggles to match.

Why This Matters for European Installers

Strategic Implications

European solar businesses should stop waiting for a 'silver bullet' policy shift and focus on operational efficiency. The US market is scaling through sheer volume; the European market will scale through smart energy management. Installers who bundle solar with heat pumps, EV chargers, and AI-driven home energy management systems (HEMS) will be the ones to survive the current market contraction. Watch for US-style 'virtual power plant' (VPP) aggregation models to cross the Atlantic—those who own the customer relationship today will be the ones to monetize grid flexibility tomorrow.