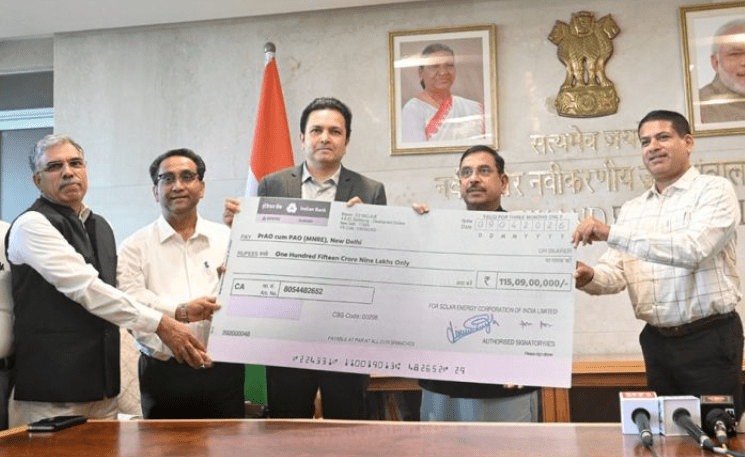

The Solar Energy Corporation of India (SECI) has presented an interim dividend of ₹115.09 crore to the Government of India for the financial year 2025-26, highlighting its significant role in the renewable energy sector.

Why it matters: Recognize that solar is maturing into a highly profitable, bankable asset class that demands professional, long-term operational excellence.

Why This Matters for European Installers

While an Indian state-owned entity paying dividends might seem geographically distant, it signals a critical shift: solar is moving from a subsidized project phase to a profit-generating maturity phase. For European solar installers, this represents the global 'normalization' of solar as a bankable, high-yield asset class. As SECI proves that large-scale renewable intermediaries can be fiscally self-sustaining, it reinforces the trend toward long-term power purchase agreements (PPAs) that are becoming the backbone of the European C&I (Commercial & Industrial) market.

Market Context and Global Implications

The Indian market is currently scaling at a pace that creates intense competition for hardware and supply chain logistics. When a central agency like SECI reports strong financial health, it attracts massive institutional capital. This influx of capital often leads to aggressive procurement strategies that can tighten the global supply of Tier-1 modules and inverters. European installers should be wary: if Indian demand continues to consume high-volume manufacturing output, supply chain bottlenecks for European SMEs could persist longer than anticipated.

What Solar Businesses Should Watch For