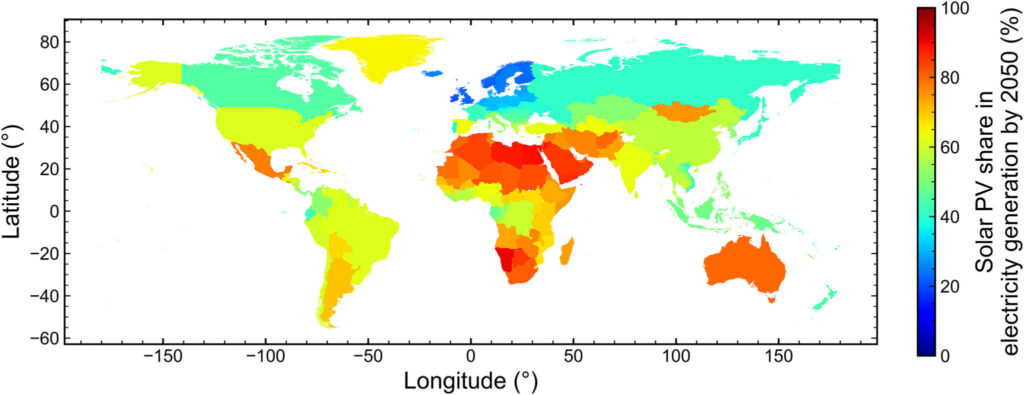

Un análisis de 60 estudios sobre energías renovables revela que, para 2050, la energía solar fotovoltaica y la eólica podrían suministrar entre el 80 % y el 100 % de la electricidad; sin embargo, las hipótesis excesivamente conservadoras sobre las inversiones de capital y los modelos fotovoltaicos simplificados suelen subestimar el potencial de implantación.

Why it matters: Pivot your business model from hardware installation to energy management services before declining CAPEX erodes your traditional hardware margins.

The Decarbonization Roadmap is Cheaper Than We Think

For European solar installers, the most critical takeaway from this research isn't the 2050 target date—it’s the realization that legacy energy models are chronically underestimating the deflationary nature of solar technology. If CAPEX continues its downward trajectory toward €166/kW, the barrier to entry for residential and commercial solar will effectively vanish, shifting the industry focus from hardware costs to energy management and storage integration.

Market Implications for Installers

What to Watch For

Keep a close eye on the Levelized Cost of Electricity (LCOE) for integrated storage solutions. As CAPEX drops, the bottleneck will move from the rooftop to the grid. Businesses that invest now in smart energy management software (EMS) and grid-balancing services will capture the next wave of profit, even if hardware margins continue to thin. Don't wait for 2050; start building the infrastructure for a high-penetration solar market today by diversifying into software-defined energy management.