Brookfield plans to exit its ₹3000 crore Bikaner solar project, highlighting investor interest in India's renewable sector.

Why it matters: Institutional investors are treating solar plants like commodities; ensure your installations are documented and 'flippable' to protect your clients' long-term ROI.

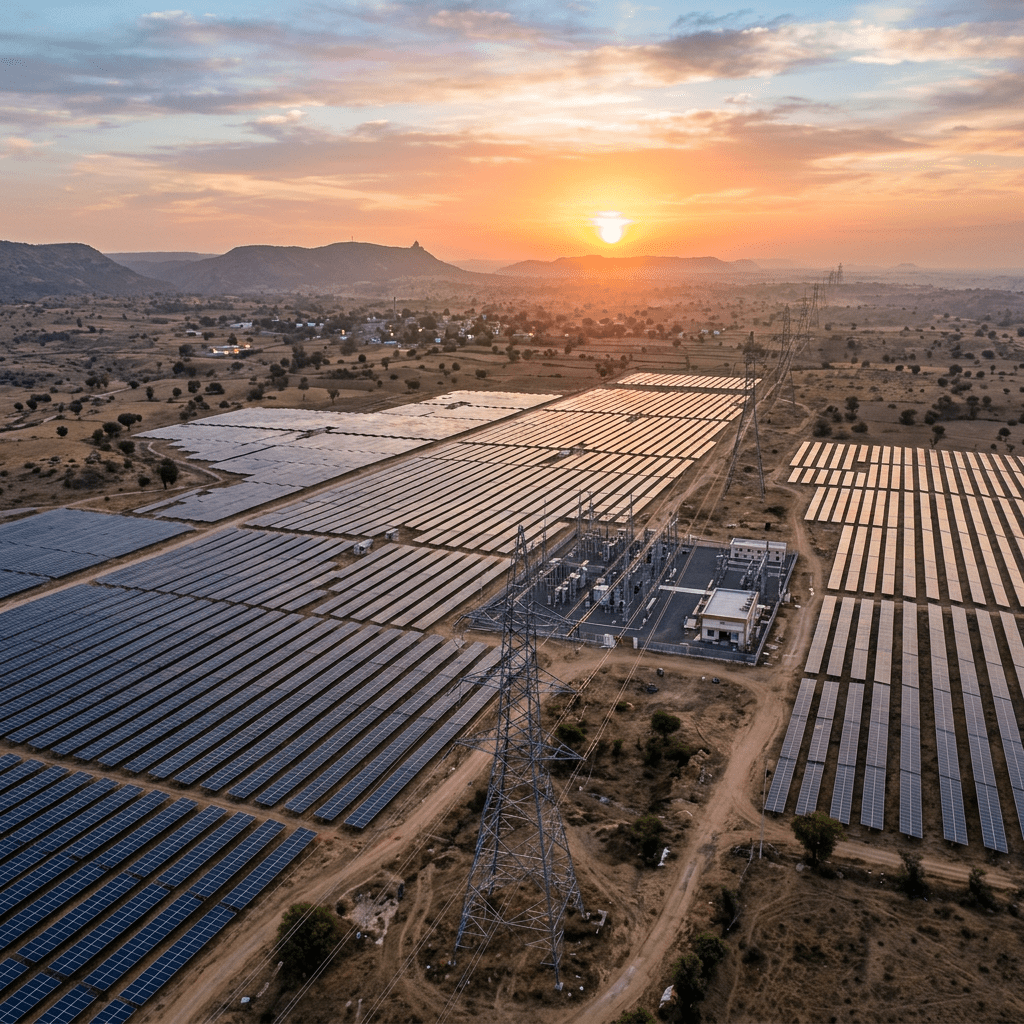

The Brookfield Playbook

Don't confuse a capital exit with a lack of confidence. When a global giant like Brookfield looks to offload a ₹3000 crore (approx. €330 million) asset like the Bikaner project, they aren't running from solar—they are cycling capital. In the European C&I market, we often get bogged down in the 'long-term hold' mentality, but Brookfield is showing us the real institutional game: build it, de-risk it, sell it to a yield-hungry pension fund, and recycle that equity into the next 500MW development phase.

Why This Should Keep You Up at Night

While Indian headlines about Vikram Solar hitting 10 GW might feel distant, they are a direct signal to your supply chain. We are seeing a massive consolidation of manufacturing capacity in non-EU markets that are aggressively protected by local RPO (Renewable Purchase Obligation) targets. Here is the reality for the European installer:

Brookfield’s exit strategy proves that in 2026, the real money in solar isn't just in the engineering; it's in the liquidity of the asset. If you are a mid-sized installer in Germany or the Netherlands, stop selling just the 'kWh output.' Start selling the 'exit-readiness' of the installation. If a project can't be bundled and flipped in five years, you’ve built a liability, not an asset.