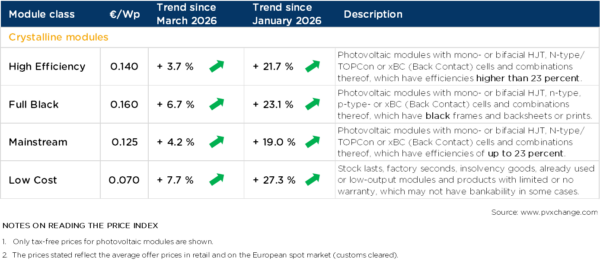

Entre marzo y abril, los precios aumentaron de media un 5,5%, siendo los módulos full black los que registraron el mayor encarecimiento.

Why it matters: Lock in your module supply now or watch your project margins vanish as the market drifts away from cheap, oversupplied inventory.

The 'Full Black' Trap

We’ve been living in a dream world of sub-€0.12/Wp pricing, but the market is correcting. That 5.5% jump isn't a blip; it’s a warning shot for anyone still quoting projects based on Q1 spot prices. The surge in 'full black' modules is particularly telling—it’s driven by residential demand in the DACH region where aesthetic mandates are non-negotiable. If you’re a developer currently sitting on a pipeline of signed contracts with fixed turnkey prices, you’re looking at a margin wipeout.

How to Survive the Squeeze

The days of 'buy when you need it' are over. We are seeing a return to 2021-style supply volatility. If your EPC firm isn't holding at least three months of inventory or doesn't have a firm forward-purchase agreement with manufacturers like Jinko or Trina, you’re effectively gambling with your company's P&L. Don't let your installation team become a victim of a procurement department that thinks price stability is a permanent feature of the market.