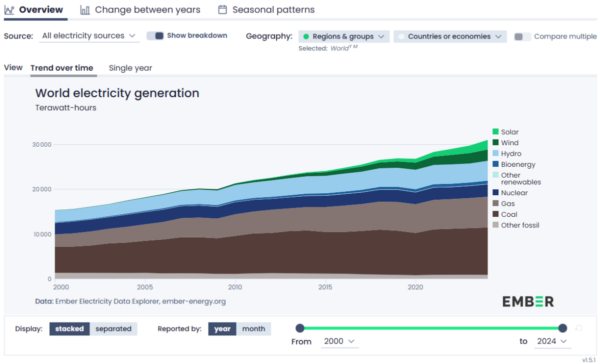

en 2025 se instalaron 814 GWdc de nueva capacidad solar y eólica, pero el ritmo de implantación de la energía eólica aumentó un 47 % interanual, frente a solo un 11 % en el caso de la energía solar.

Why it matters: Solar’s growth is slowing while wind scales; stop selling raw PV capacity and start selling grid-integrated, dispatchable energy systems.

The Solar Dominance Plateau

Don't be fooled by the raw volume of PV deployment. When you see solar growing at 11% while wind surges at 47%, the wind isn't just 'gaining ground'—it’s signaling a structural shift in how European grids will prioritize capacity. For a decade, solar installers have enjoyed the 'low-hanging fruit' era: easy permits, cheap modules from Jinko or Trina, and high retail electricity prices. That era is hitting a wall.

The Cannibalization Problem

If you are still selling pure-play solar projects in the Netherlands or Southern Germany without an integrated BESS strategy, you are building your own obsolescence. The 4:1 solar-to-wind ratio is exactly what leads to negative midday pricing. When the spot price hits zero—or goes negative—because your 50MW PV park is dumping power at the same time as the neighbor's, your ROI goes out the window.

The market is shifting from a 'volume' game to a 'grid-value' game. The installers who thrive won't be the ones with the cheapest racking system, but the ones who can guarantee a PPA that stays profitable when the solar midday glut turns into a price bloodbath.