Solar PV accounted for more than a quarter of total global energy demand growth in 2025, becoming the single largest contributor to new energy supply, according to the International Energy Agency.

Why it matters: Volume is at an all-time high, but profit per watt is hitting an all-time low — stop selling panels and start selling storage-backed energy management.

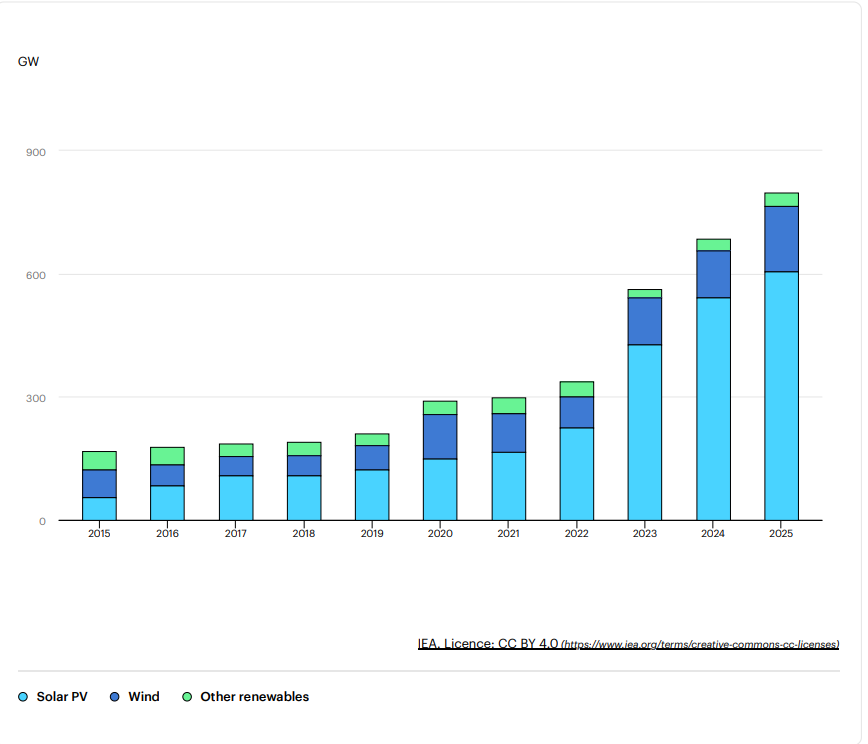

The Volume Illusion

So, the IEA is popping champagne because the world added 600GW of PV in 2025. If you're an installer in Hamburg or a distributor in Milan, stop looking at these global headlines. This data is the ultimate vanity metric. Massive deployment numbers don't pay the overhead when the market is flooded with Tier-3 modules and inverter lead times have vanished.

The Real Story is Value, Not Volume

We are seeing a brutal disconnect between capacity growth and project profitability. When 600GW hits the grid, cannibalization is no longer a theoretical risk—it’s a daily reality for your C&I clients. If your portfolio is still 100% solar, you’re selling a commodity that is increasingly worthless at noon. The math is simple:

The manufacturers—Sungrow, Huawei, and the endless sea of Chinese module makers—are pushing for scale to survive the margin compression. But for the European installer, the '600GW' era means your competitive advantage has shifted from 'who can install the fastest' to 'who can manage the most sophisticated energy arbitrage software.' If you’re still pushing standard grid-tied residential systems without a strategy for dynamic tariffs or load shifting, you’re building yesterday’s business model in a market that has already moved on.