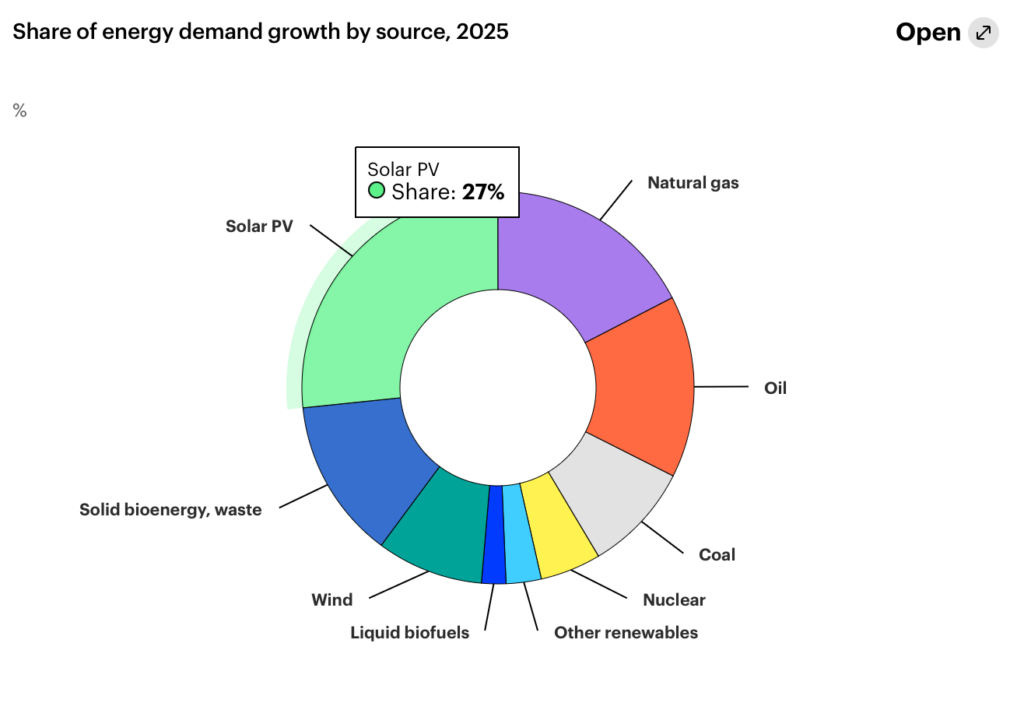

Los datos de 2025 presentados por la AIE evidencian que el sistema energético global ha entrado en una fase en la que las renovables, con la solar a la cabeza, lideran la expansión de la oferta y comienzan a desplazar de forma estructural a los combustibles fósiles.

Why it matters: Grid prices are decoupling from gas; if your PV proposals don't include storage as a standard component, you're building stranded assets.

The Transition Just Left the Paper Phase

Let’s cut the fluff: the IEA confirming solar has structurally displaced gas as the primary growth driver isn't just a headline for bureaucrats in Brussels. For an installer in Bavaria or a developer in Andalusia, this is the final nail in the coffin of the 'baseload' argument. If you are still selling PV systems based on simple ROI calculations against grid parity, you are leaving money on the table.

The Margin Shift

When gas is structurally sidelined, market volatility changes. We aren't looking at a slow 2% increase in demand; we are looking at a market where the *marginal cost* of electricity is increasingly defined by solar output. For your C&I clients, this means:

Stop pitching 'panels on the roof.' Start pitching 'energy management systems.' The grid is becoming a backup, not a partner. If you aren't integrating smart energy management—think SMA’s Sunny Portal or Fronius’s ecosystem—to optimize local consumption during those 27% growth periods, your competition will. The shift from gas isn't a future scenario; it's the current reality of the PPA market. If you can’t show a client how to buffer against 0€/MWh clearing prices during peak solar hours, you're going to lose the deal to someone who can.