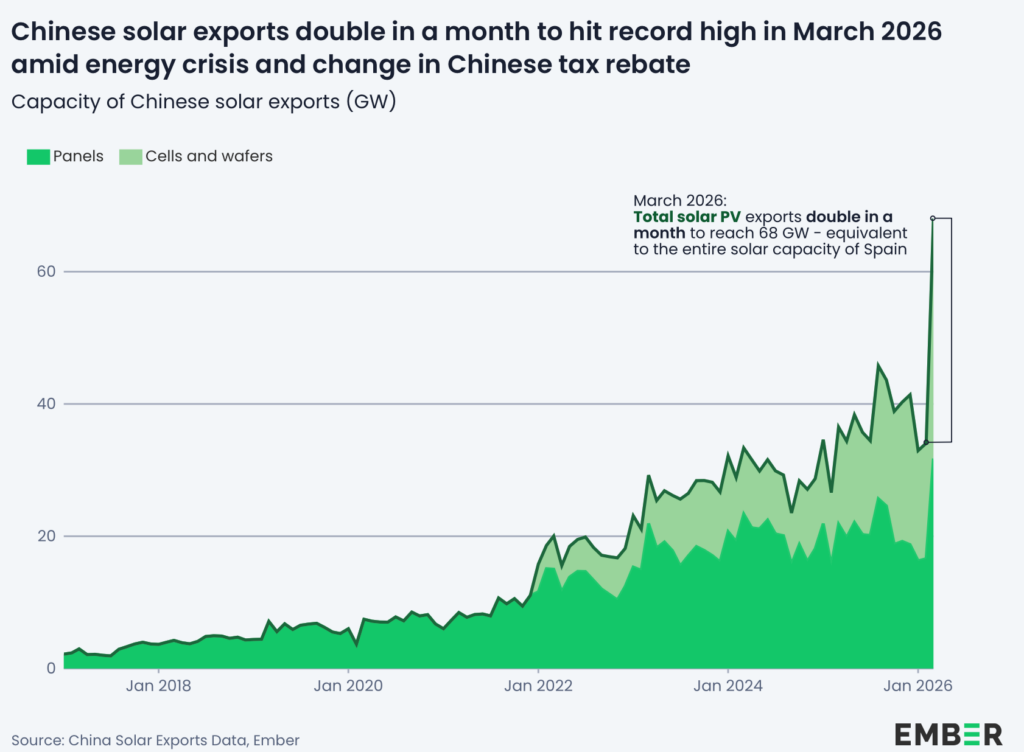

Las exportaciones de células y obleas (36 GW, +108% mensual) ya superan a las de módulos (32 GW, +91%), lo que indica una creciente deslocalización del ensamblaje final hacia mercados regionales.

Why it matters: Your 'European' modules are likely just Chinese cells in a local frame—don't pay a premium for a sticker without verifying the cell source.

Stop patting yourselves on the back for supporting "local" manufacturing. The latest data from China isn't just a record; it’s a revelation of how the global solar shell game is played. For the first time, China exported more upstream components (wafers and cells) than finished modules. This 36 GW flood of semi-finished goods tells us exactly where the Net Zero Industry Act (NZIA) is headed: toward a future of glorified screwdriver factories.

The Mirage of European Independence

While EU politicians dream of a 30 GW domestic supply chain by 2025, the reality on the ground in places like Turkey or even the few remaining assembly lines in Germany and Poland is that we are deeper in China's pocket than ever. If you're buying a "European-assembled" module today, you aren't buying European energy security; you’re buying a Chinese TOPCon cell that was popped into a frame in a warehouse outside of Wrocław or Istanbul to bypass trade sensitivities or qualify for local-content subsidies.

The Margin Trap for Installers

As an installer, you need to look at the numbers: cell and wafer exports grew by 108% in a month. This massive oversupply is why module prices are languishing at €0.10-€0.12/Wp. If your distributor is trying to sell you a "Made in EU" premium that’s 50% higher than a Tier-1 Chinese brand, ask for the Bill of Materials (BOM). If the cells are from Tongwei or JA Solar, that premium is pure marketing fluff with zero supply chain de-risking. We saw what happened when Meyer Burger pivoted to the US—local assembly is fragile; the cell is where the power (and the risk) sits.

The Real Signal

This isn't de-globalization; it's the logistical optimization of Chinese dominance. Shipping wafers is cheaper and lower-risk than shipping glass-heavy modules. If you aren't pricing your 2025 C&I projects based on the assumption that upstream costs will remain depressed regardless of EU trade barriers, you're leaving money on the table. The dragon isn't retreating; it's just changing clothes.