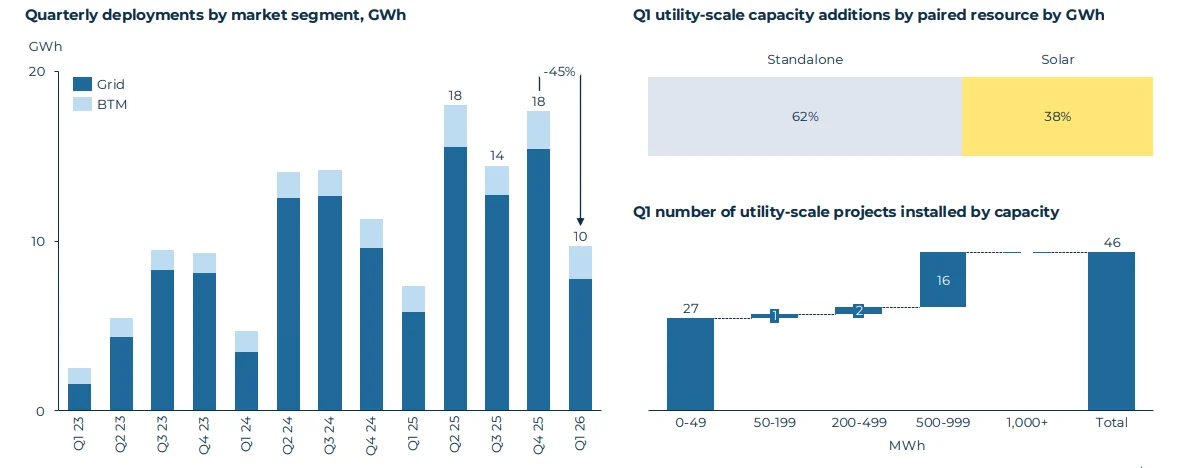

The US installed 9.7GWh of new battery energy storage system (BESS) capacity, according to the US trade association group, the Solar Energy Industries Association (SEIA).

Why it matters: Massive US BESS volume will cannibalize LFP cell availability and kill the 'wait-for-lower-prices' strategy for European installers.

When the US utility-scale market sneezes, European installers catch a cold. Seeing 9.7GWh dropped into the ground in a single quarter isn't just a "big number"—it’s a signal that the global LFP supply chain is being sucked into a North American vacuum. For context, this single quarter roughly matches what the entire European residential storage market managed in all of 2023. If you're a developer in Oberhausen or a wholesaler in Rotterdam, you need to stop looking at US news as a distant curiosity and start looking at it as your primary procurement risk.

The LFP Vacuum Effect

The vast majority of this capacity is built on LFP (Lithium Iron Phosphate) chemistry, largely sourced from the same Tier 1 Chinese manufacturers—think CATL, BYD, and EVE Energy—that supply the European C&I and residential sectors. When developers like NextEra or Vistra lock in multi-gigawatt-hour master supply agreements to hit these Q1 numbers, they move to the front of the queue. Your 500kWh C&I project in Flanders? You're an afterthought. We’ve seen this pattern before: when US demand spikes, lead times for European 'white label' or second-tier battery brands suddenly stretch from 8 weeks to 24.

The Price Floor is Hardening

While we've enjoyed a slide in cell prices toward the $50/kWh mark, this volume of deployment creates a structural floor. You cannot expect further aggressive price cuts in the EU market while the US is demonstrating this level of absorption capacity. If you are sitting on a project proposal waiting for 'one more price drop' before signing the contract, you are playing a dangerous game. With the Red Sea shipping volatility adding a €0.02-€0.05/Wh premium on logistics to Europe, the massive US volume ensures that manufacturers have zero incentive to discount for the fragmented European market. Bottom line: Lock in your 2026 supply contracts now, or prepare to explain to your customers why their BESS unit is stuck on a wharf in Ningbo while the Americans hog the supply.