El 16 de junio publicarán las solicitudes admitidas, el 24 del mismo mes se abrirán las ofertas económicas y la adjudicación está prevista para los primeros días de julio.

Why it matters: Mega-tenders in emerging markets suck up global tier-1 battery supply, meaning your 2025 project lead times just got riskier.

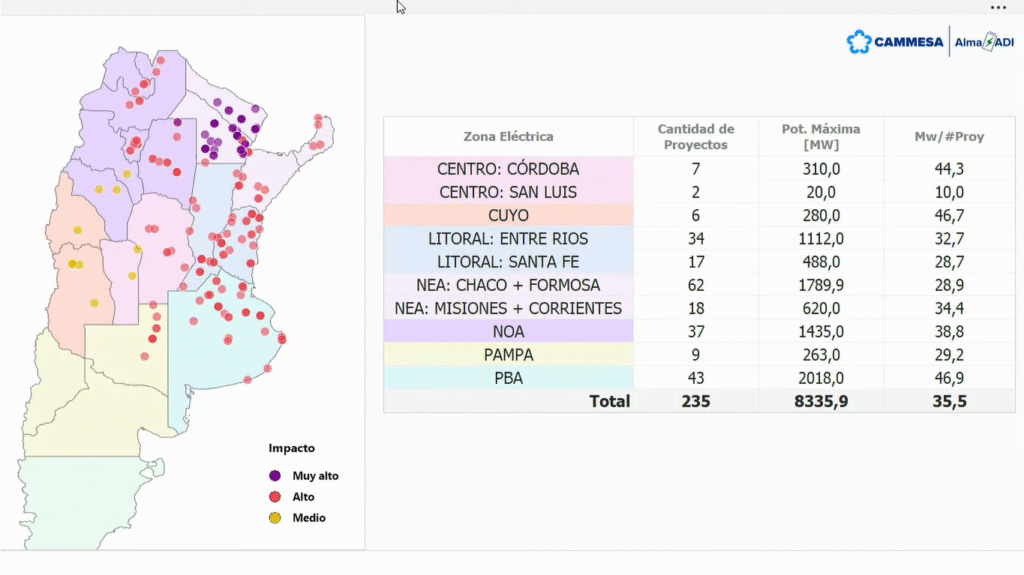

When a country with a credit rating as volatile as Argentina’s receives 235 bids for 8.3 GW of storage, the global BESS market isn't just maturing—it’s hitting a fever pitch. For the European installer or developer, this isn't just a curiosity from the southern hemisphere; it is a direct threat to your 2025-2026 supply chain stability.

The Global Vacuum for LFP Cells

Let’s talk about the math. 8.3 GW of bids, even if only partially adjudicated, represents a massive pull on the global supply of Lithium Iron Phosphate (LFP) cells. While EU professionals are focusing on the Net-Zero Industry Act and domestic manufacturing, the reality is that tier-1 manufacturers like CATL, BYD, and Sungrow follow the volume. A sudden 8GW demand signal from South America creates a procurement vacuum. If you are a mid-sized EPC in Germany or Italy thinking you can buy BESS containers 'off the shelf' next year without a master supply agreement, you are dreaming.

Why Argentina Matters to a Spanish Developer

The technical challenges in Argentina—aging transmission lines and high curtailment in the northern PV hubs—mirror the issues we are seeing in Iberia and parts of Eastern Europe. This tender is a massive 'stress test' for large-scale BESS in high-inflation environments. If developers can make the ROI work in a country where the cost of capital is stratospheric, it proves that the ancillary services and arbitrage model is now bulletproof. We’ve seen this pattern before: when mega-tenders succeed in emerging markets, the technology providers pivot their best engineering support and quickest lead times to those 'whale' projects, leaving European C&I projects fighting for scraps.

The Bottom Line on Margin

Expect this volume to keep global battery prices from bottoming out as fast as some analysts predict. For your next 5MW C&I pitch, don't just sell the hardware; sell the secured delivery slot. If you don't have a direct line to a manufacturer or a very large distributor, you're going to get squeezed by projects like these half a world away.