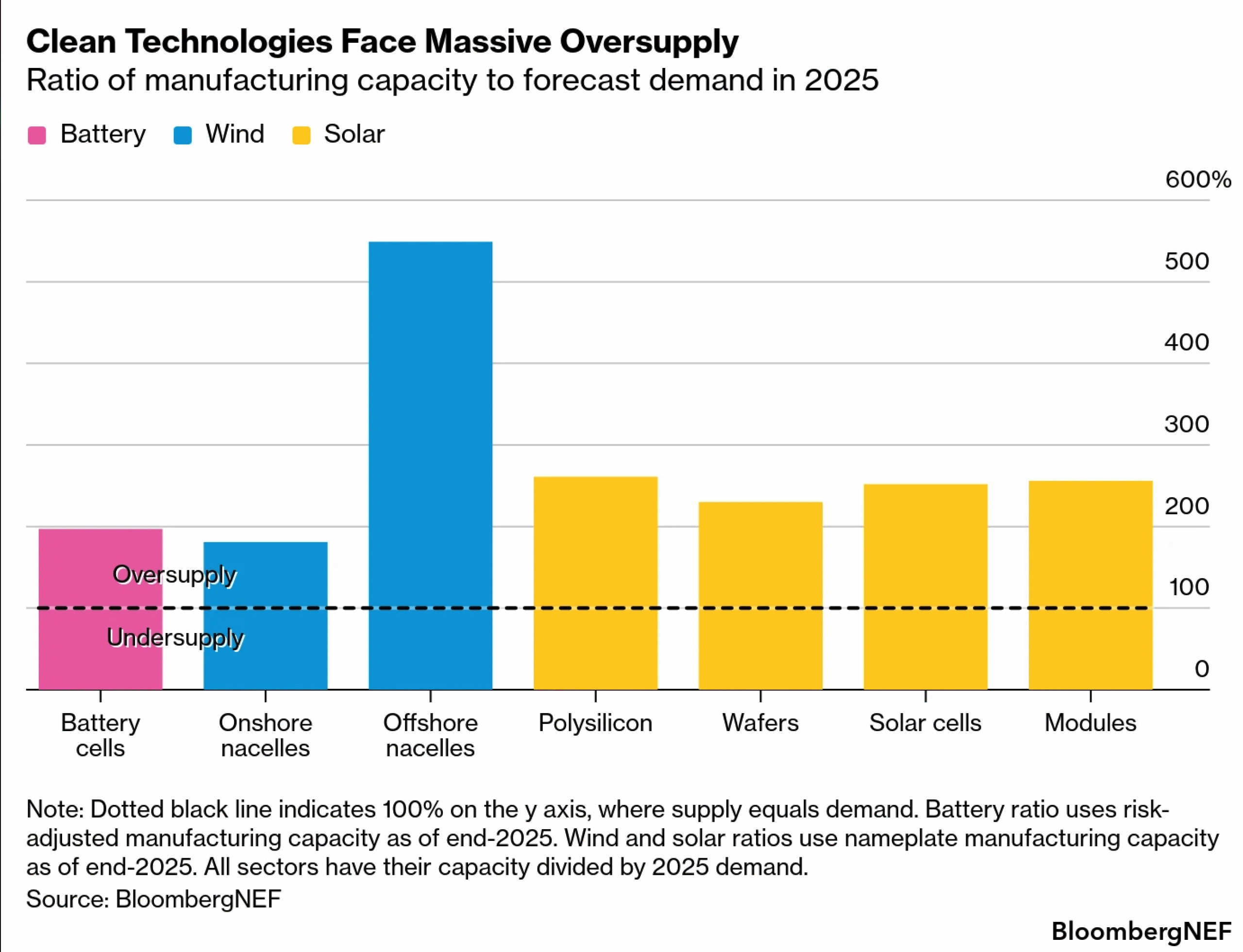

Actualmente, según BNEF, existe más del doble de capacidad manufacturera necesaria para cubrir la demanda global en buena parte de la cadena de valor solar, eólica y de baterías, lo que continúa presionando los márgenes de los fabricantes.

Why it matters: Record-low hardware prices are permanent for the foreseeable future, so pivot your business model from 'securing components' to 'maximizing system intelligence' before your competition does.

The Great Margin Massacre

Let’s stop pretending the $479 billion trade figure is a sign of a healthy, balanced market. For anyone sitting in an office in Berlin, Madrid, or Utrecht, that number represents a brutal, Darwinian struggle for survival among manufacturers. When BNEF tells us there is double the capacity needed to meet global demand, they aren't just talking about a surplus; they are describing a structural inventory dump that has driven module prices below €0.11/Wp for standard TOPCon kits.

If you’re an installer, this is your golden era of procurement. You are effectively being subsidized by the negative margins of Chinese giants like LONGi and JinkoSolar. However, this 'gift' comes with a massive liability tail. In a market where supply is 2x demand, the weakest players—and even some mid-tier veterans—will vanish. We’ve already seen the casualties in the European manufacturing sector, with Meyer Burger halting production in Germany because they couldn't compete with the flood of cheap silicon.

The Installer’s Arbitrage Checklist

Don't just celebrate the low CAPEX on your next C&I project. You need to play this glut strategically:

The EU’s Net-Zero Industry Act (NZIA) wants 40% local production, but until it can bridge the massive price gap created by this 2x capacity surplus, it’s just a paper tiger. Your job is to leverage these global tensions to lower LCOE for your clients while ensuring you don't tether your reputation to a manufacturer that won't exist in 2026.