Managers of the UK’s largest BESS owner-operator Gresham House Energy Storage Fund (GRID) discussed recent investment news and future strategy this week.

Why it matters: The UK's storage pioneer is struggling, proving that 'passive' battery investment is dead; if your project doesn't have a sophisticated trading strategy, it's a stranded asset.

If you want to know what the future of large-scale storage looks like in Germany, Italy, or the Netherlands, look at the bruises on Gresham House (GRID). As the UK’s largest BESS owner-operator, they’ve spent the last year in a brutal masterclass on merchant risk. For years, BESS developers sold investors a dream of 'easy' revenue from frequency response (FFR/Dynamic Moderation). But as soon as the market saturated, those margins evaporated, leaving funds like GRID scrambling to make sense of the Balancing Mechanism (BM).

The 'Skip Rate' Scandal

The hard truth for any EPC or developer moving into the 5MW+ space is that hardware is now a commodity, but dispatch is a battlefield. In the UK, National Grid ESO has been 'skipping' batteries in favor of gas peakers even when batteries were cheaper. GRID’s struggle proves that even with 740MW+ of operational assets, you are at the mercy of the grid operator’s legacy software and manual processes. If you are pitching a C&I project in the EU based on 2023 ancillary service prices, you are lying to your client.

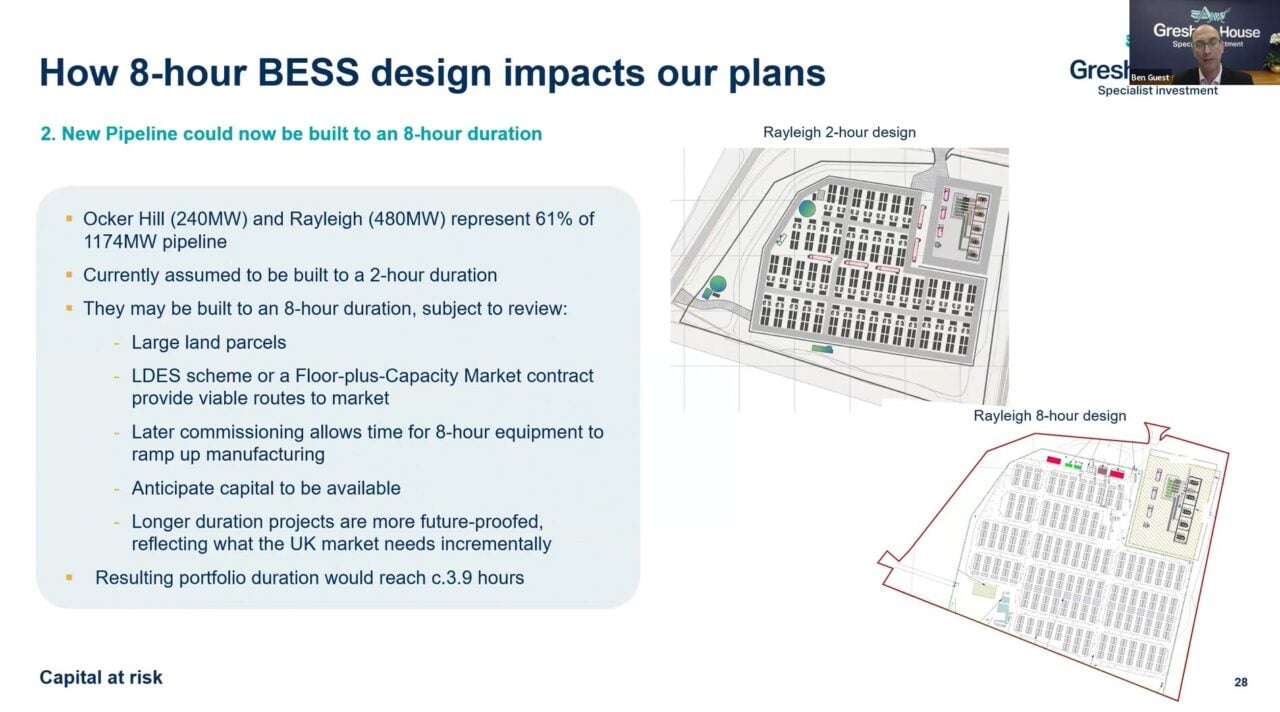

The Shift to Trading and Duration

What is GRID doing to survive? They are moving toward 2-hour duration and sophisticated trading. This is the blueprint for the continent. We are moving away from the 'set and forget' battery model. To make a project bankable in 2025, you need to show:

The UK is not a special case; it is the crystal ball for the rest of Europe. The saturation that hit GRID will hit the German market next as the 'Solar-plus-Storage' gold rush continues.