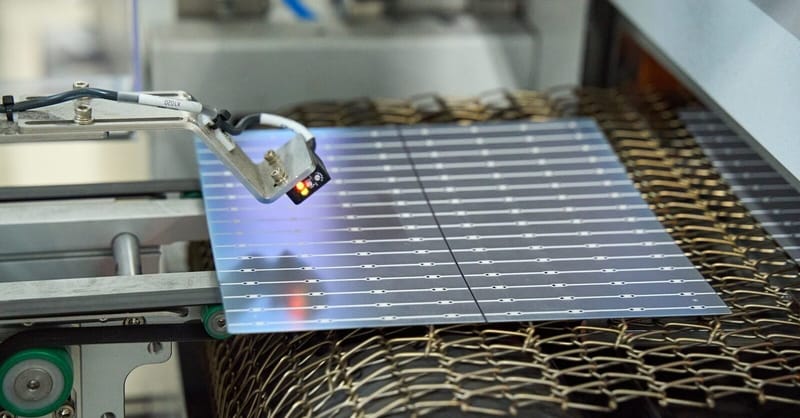

Qcells has officially begun commercial production of silicon solar cells at its factory in Cartersville, Georgia, the company said Tuesday. That factory is the largest of its kind in the country — and a long-awaited boost to the U.S. solar supply chain.

Why it matters: Hanwha’s pivot to the US means European installers should expect tighter allocations and higher premiums for QCells as the company prioritizes the lucrative IRA-backed American market.

The Great Transatlantic Drain

While European regulators are still busy debating the fine print of the Net-Zero Industry Act (NZIA), Hanwha QCells has just finished building a cathedral to the Inflation Reduction Act (IRA). The Cartersville facility isn’t just a factory; it’s a loud signal that the solar manufacturing center of gravity is shifting toward the dollar, not the euro. For an installer in Essen or Lyon, this matters because capital is finite. When a Tier-1 giant like QCells pours billions into Georgia, they aren't just building cells; they are building a preferred relationship with the US utility-scale market.

The Subsidy Math That WinsThe 45X Advanced Manufacturing Production Credit in the US provides a direct, bankable tax credit for every watt produced. In Europe, we offer complex grant structures and 'Resilience Auctions' that vary by member state. Look at the carnage: Meyer Burger effectively shuttered Freiberg to chase the US carrot. If you’re banking on a 'Made in Europe' QCells module to satisfy a local content requirement in a French or Italian tender, you’re looking at the wrong map. Hanwha is chasing the 10% domestic content bonus in the US, which makes their modules virtually unbeatable in the American C&I sector.

As an EPC, your takeaway is simple: the 'reliable' supply chain you've counted on from Hanwha is now a two-headed beast, and the American head is getting fed much better. If you’re signing multi-year procurement frameworks, you need to ask your distributor exactly where your 2025/2026 allocations are physically coming from. If the answer is 'we're waiting for EU subsidies to kick in,' start looking for a Plan B.