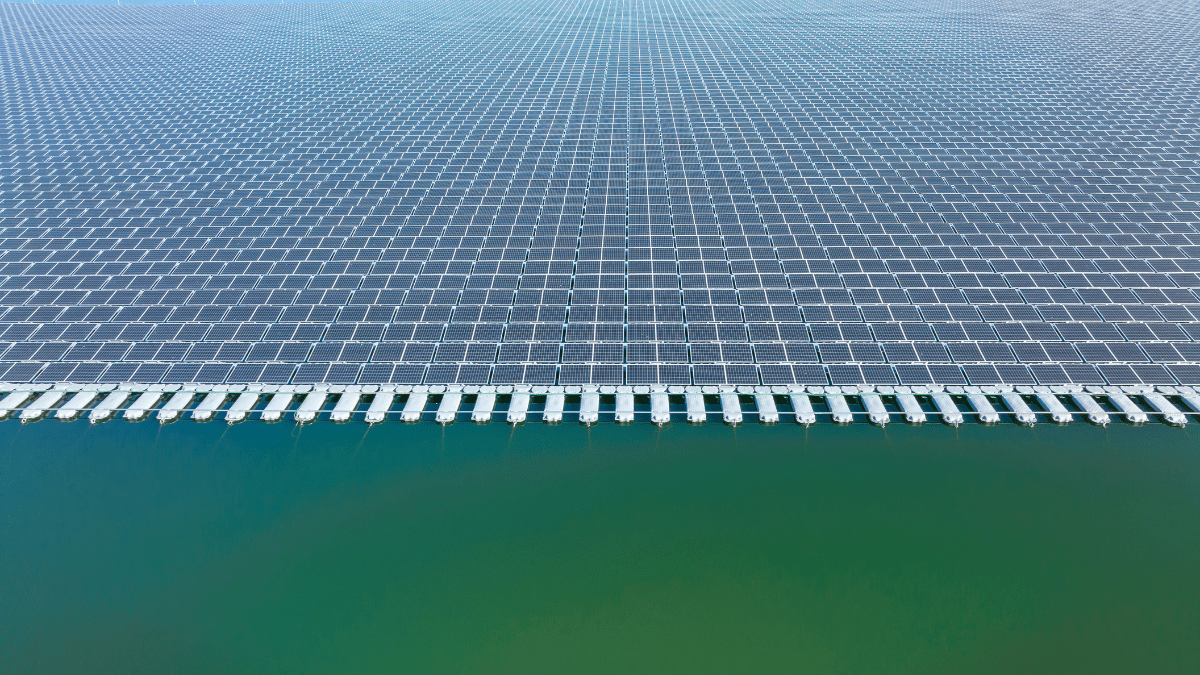

The National Institute of Solar Energy's report reveals India's floating solar photovoltaic potential at 102.18 GWp, offering a solution for renewable energy expansion with minimal land use.

Why it matters: India’s massive FPV pipeline will dictate global floatation costs—if you're not tracking their scale, your project's CAPEX estimates are already obsolete.

While European developers are still haggling over environmental impact assessments for 5MW ponds in the Netherlands, India is laying the cartographic groundwork for a 102.18 GWp FPV gold rush. This isn't just a big number; it’s a strategic pivot that highlights Europe’s biggest FPV bottleneck: permitting and scale, not technical potential.

The Hybrid Advantage We're Missing

India’s focus on integrating FPV with existing hydropower infrastructure is the real money angle. By utilizing the existing grid connections of hydro plants, they bypass the €100k+/km interconnection costs that frequently kill small-to-mid-scale European projects. For an installer in Germany or Poland, the lesson is clear: stop looking at standalone ponds and start scouting brownfield industrial reservoirs and existing hydro assets where the infrastructure already exists. The first person to pitch a hybrid PPA to a utility with an aging dam wins the next decade.

Scale Will Brutalize Component Pricing

When India starts commissioning at this scale, the cost of high-density polyethylene (HDPE) floats and specialized anchoring systems from players like Ciel & Terre or Sungrow will be dictated by Asian demand. If you're planning an FPV project in Portugal or Italy for 2026, your margins are currently at the mercy of India's procurement cycle. We saw this with bifacial modules; we’ll see it again with floating racking.