ACEN Corporation plans to divest up to a 49% stake in a 250 MW solar project in Rajasthan, India, as part of its capital recycling strategy to enhance future growth and investments.

Why it matters: Institutional money wants de-risked assets; if you're not planning your exit before you break ground, you're just an EPC with a hobby.

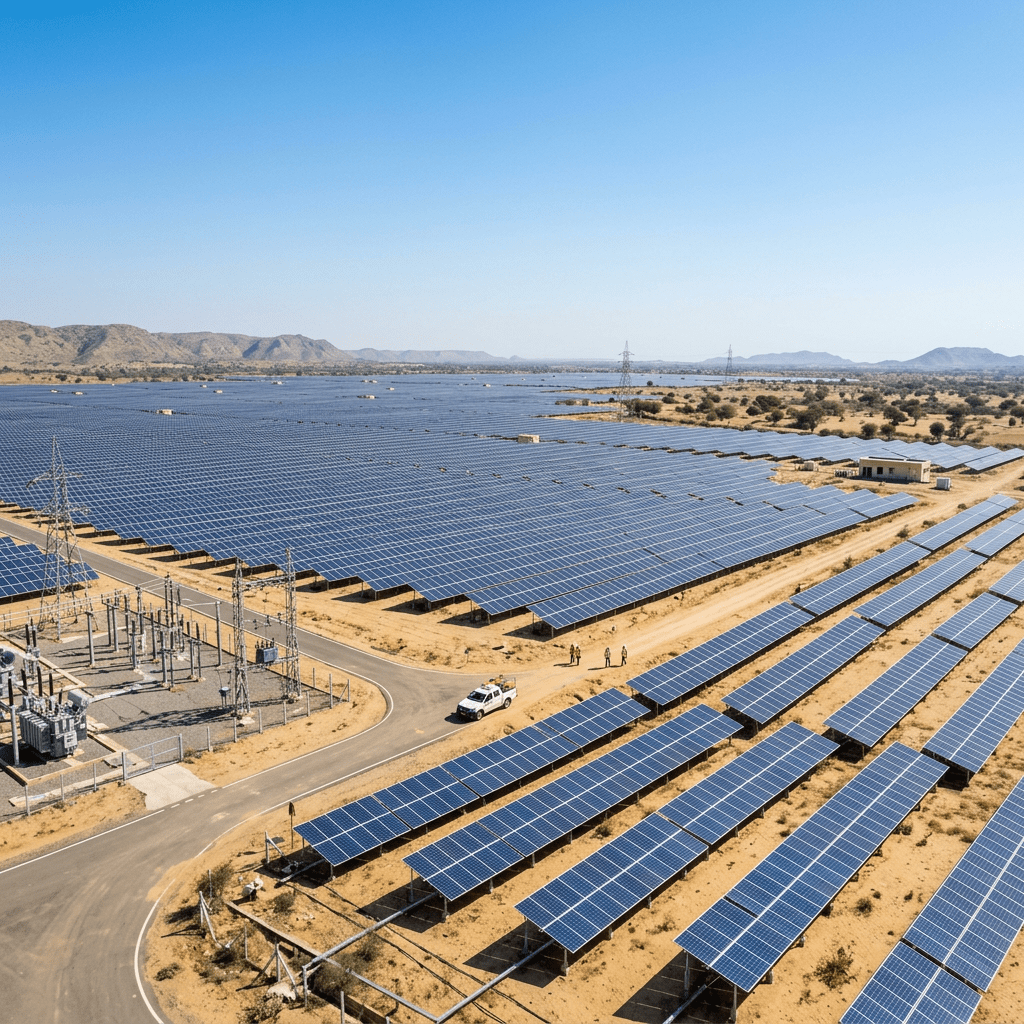

The Great Recycling Act

If you're still building projects with the intention of holding them for 25 years, you’re playing a 2015 game in a 2024 market. ACEN’s move to offload 49% of their 250 MW Rajasthan asset to a Mitsubishi subsidiary (Diamond India Renewables) isn’t a sign of weakness—it’s a masterclass in capital recycling. By selling nearly half the equity once the project is de-risked, they’re pulling their initial "sweat equity" out to hunt for the next 500 MW.

Why the Rajasthan-to-Rotterdam Link Matters

For a developer in Spain or Poland, the logic is identical. The cost of capital (WACC) for a developer is usually 8-10%, while for a massive conglomerate like Mitsubishi, it might be 4-6%. It is mathematically irresponsible to keep 100% of a completed, operational asset on a developer’s balance sheet when a yield-hungry giant will pay a premium for the steady cash flow. We’re seeing this exact pattern with Statkraft and Iberdrola selling minority stakes in offshore wind and massive PV clusters to sovereign wealth funds to keep their balance sheets lean.

European professionals should take note: the build-to-sell model is migrating from utility-scale down to the 5-20 MW C&I portfolio level. If you aren't bundling your projects to sell to institutional investors, you're missing the real profit margin in this industry.