The annual ITRPV report was published this week, offering a snapshot of the latest technological trends shaping the industry.

Why it matters: The 'cheaper solar' narrative is hiding a massive shift to n-type modules that will make your current inventory and technical knowledge obsolete by next season.

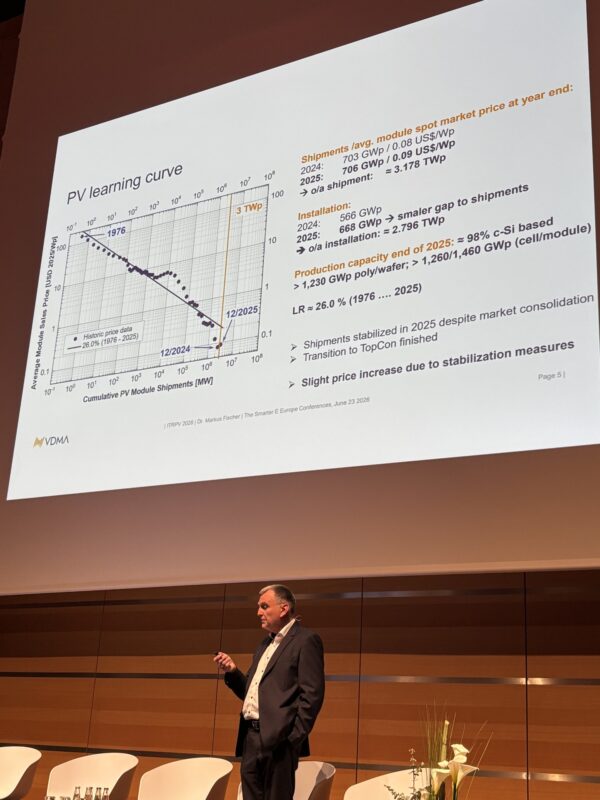

The ITRPV learning curve is the most beautiful chart in clean tech—unless you’re the one holding €2 million in devaluing inventory. While the report celebrates the relentless drop in costs per watt-peak, for the European installer, this "historic learning curve" is a double-edged sword. We are witnessing the brutal transition from p-type PERC to n-type technologies (TOPCon and HJT) happening faster than the supply chain can breathe. If your warehouse is still stacked with 400Wp PERC modules, you’re not looking at an asset; you’re looking at a liability.

The Efficiency Trap

The report highlights that n-type cells are now the baseline, not the premium. We’re hitting 23-24% module efficiency as a standard. However, the hidden cost for project developers isn't in the modules—it’s in the lack of mechanical standardization. As manufacturers chase the learning curve by tweaking wafer sizes (M10 to G12 and the confusing G12R variants), mounting system compatibility is becoming a nightmare. I’ve seen crews on-site in the Netherlands forced to re-drill rails because a manufacturer changed frame dimensions by 15mm mid-shipment to shave a few cents off their BoM.

The Silver Bullet (or Lack Thereof)

One metric in the ITRPV that every business owner should highlight is silver consumption. The industry is desperately trying to pivot to copper plating or 'super-multibusbar' designs to de-risk. With silver prices volatile, a sudden spike could decouple module prices from the learning curve overnight. If you’re quoting 2026 PPA projects today based on these 15-year historical averages, you’re gambling on Chinese material science staying ahead of global commodity inflation. Don't bet the farm on linear price drops.