El verdadero límite de la energía solar no depende de la cantidad de radiación o de superficie disponible en un país, sino de hasta qué punto la generación fotovoltaica coincide con la demanda eléctrica hora a hora.

Why it matters: The era of 'set it and forget it' solar is over; if you don't integrate storage and demand response, price cannibalization will kill your clients' ROI.

The Cannibalization Trap

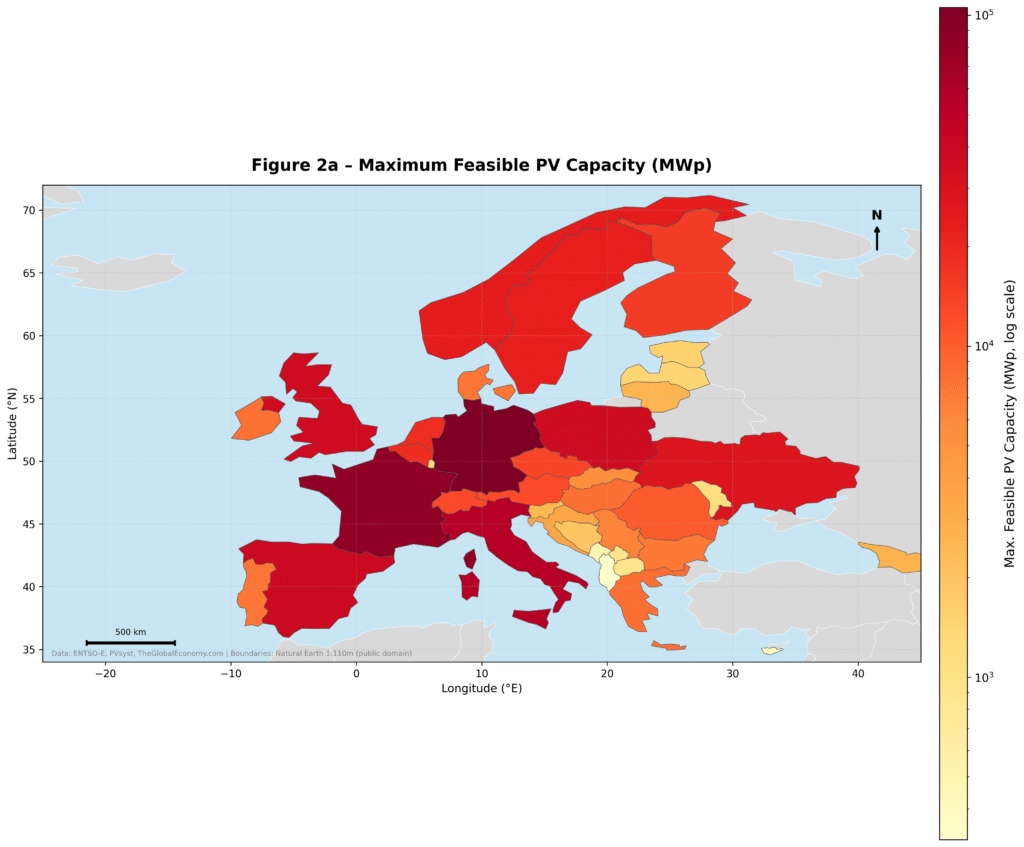

This 614 GW figure isn't a victory lap; it’s a warning. While the industry loves to boast about installation records, we are rapidly approaching the point where 'dumb' solar—PV without storage or flexible demand—becomes its own worst enemy. In markets like Spain and the Netherlands, we’re already seeing the 'duck curve' turn into a 'canyon curve.' If you’re a developer still pitching projects based on a flat €/kWh return without accounting for price cannibalization at 1:00 PM, you’re selling a fantasy.

The Math of Survival

The study suggests we can integrate 614 GW before hitting a wall, but for the boots on the ground, the wall is already here. In Germany, negative pricing events are no longer an anomaly; they are a structural feature of the market. When the grid is saturated, your 100kW C&I project isn't an asset; it’s a liability that the TSO (Transmission System Operator) might curtail without compensation. The real opportunity isn't in hitting that 614 GW limit; it's in the flexibility gap. Every MW of PV you install now should be paired with a BESS (Battery Energy Storage System) or at least be 'storage-ready' with a sophisticated EMS (Energy Management System).

Moving the Goalposts

We need to stop talking about 'installed capacity' and start talking about 'shorthanded demand.' Under EU RED III (Renewable Energy Directive), the pressure to decarbonize is immense, but the grid can't swallow 600+ GW of intermittent energy without a massive shift in how we sell. If you are an installer, your sales pitch needs to evolve from 'save on your bill' to 'arbitrage the volatility.' Companies like SMA and Huawei are already pivoting their hardware to prioritize grid-forming capabilities and hybrid integration. If you aren't talking to your clients about shifting their heavy loads—like industrial cooling or EV fleet charging—to coincide with that 614 GW peak, you’re leaving money on the table and building a fragile grid.