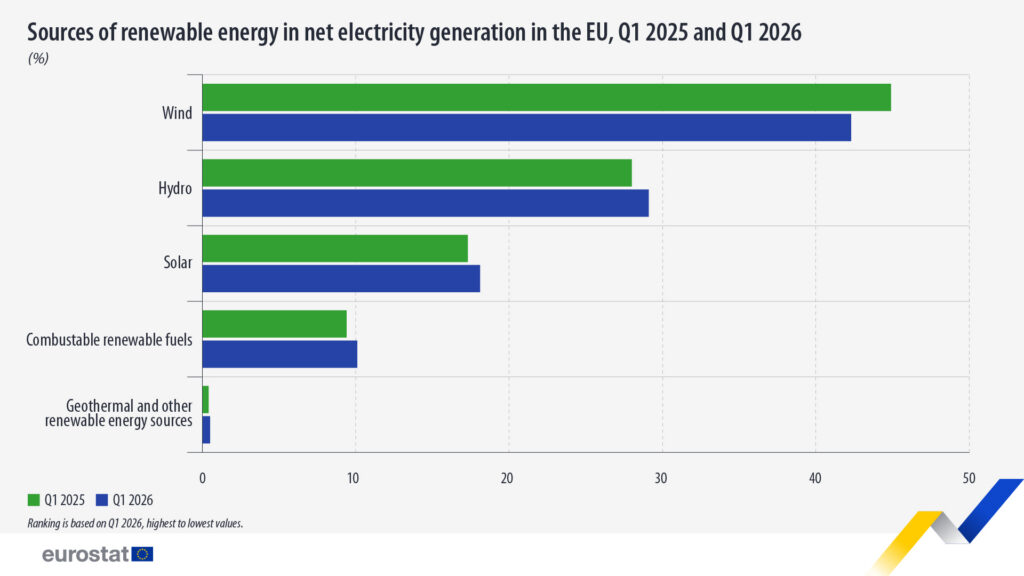

La energía solar representó el 17,3% de toda la electricidad renovable generada en la UE durante el T1 2026, consolidándose como la tercera fuente renovable del bloque, por detrás de la energía eólica y la hidráulica.

Why it matters: If you aren't selling curtailment-ready systems with EMS, your portfolio is a ticking clock of negative price exposure.

Let’s look past the press release fluff about "milestones." If solar is accounting for 17.3% of the renewable mix in Q1—traditionally the weakest quarter for irradiance—we are staring down the barrel of a massive oversupply crisis for the summer months. For any installer or developer from Seville to Szczecin, this isn't just a growth statistic; it’s a signal that the merchant model is fraying at the edges.

The Price Cannibalization Trap

When solar reaches these levels during the low-demand winter and early spring, the "duck curve" doesn't just sag; it bottoms out. We’ve seen this play out with Red Eléctrica in Spain and Tennet in the Netherlands: as soon as the sun hits its zenith in Q2 and Q3, spot prices will crater to zero or go negative. If you are building C&I projects without integrated storage (BESS), your customers’ ROI is going to vanish during peak production hours.

The vanity metrics from Brussels hide a hard reality for the field. The 17.3% share in Q1 proves that the physical capacity is there, but the market flexibility is not. We are no longer in the business of generating electrons; we are in the business of managing them. If your 2026 strategy still relies on high feed-in premiums or stable spot prices, it’s time to rewrite the playbook.